"Nobody is guilty of anything." Roman Goryunov. Director of PAO "SPB Exchange" It is this quote from Goryunov that best characterizes in a satirical key the narratives of the financial regulator of the Russian Federation regarding the most grandiose financial scam in the Russian Federation since the robbery of the people by Sberbank of the USSR. Details - on the telegram channel VChK-OGPU and Rucriminal.info.

The history of the Russian stock exchange since the transition to a market economy goes back many years, but the financial market really turned around at full capacity in 2021 not only as a result of massive advertising by opinion leaders from Ksenia Sobchak to Artemy Lebedev, loyal info-guardians of any Kremlin policy, but also because on October 21, 2021, the director of the St. Petersburg Stock Exchange Roman Goryunov happily announced direct access to the New York Stock Exchange (hereinafter NYSE) through the custodian bank Bank of New York Mellon (hereinafter BONY), which made it possible to reduce the commission for buying and selling securities to negligible ones.

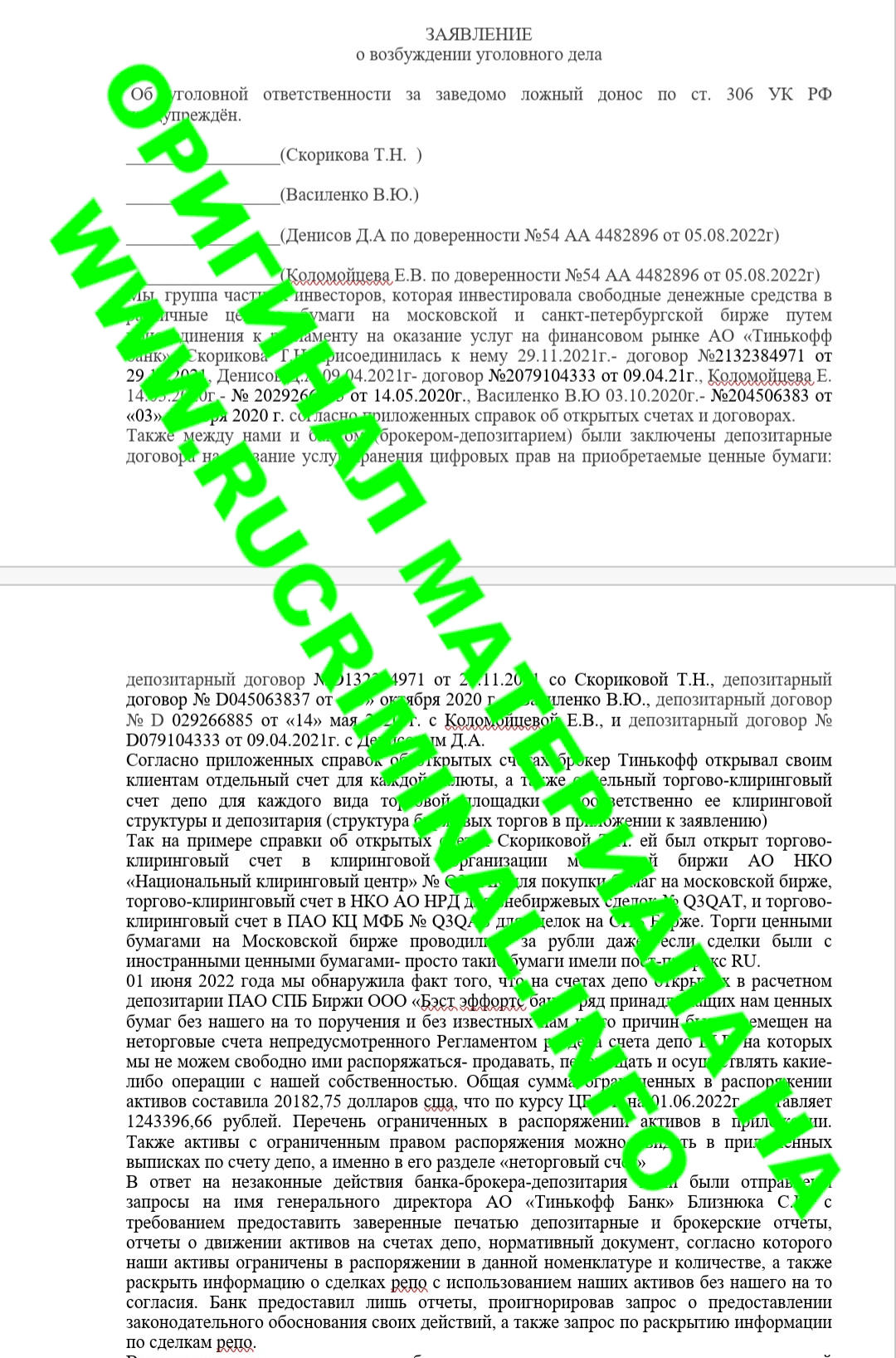

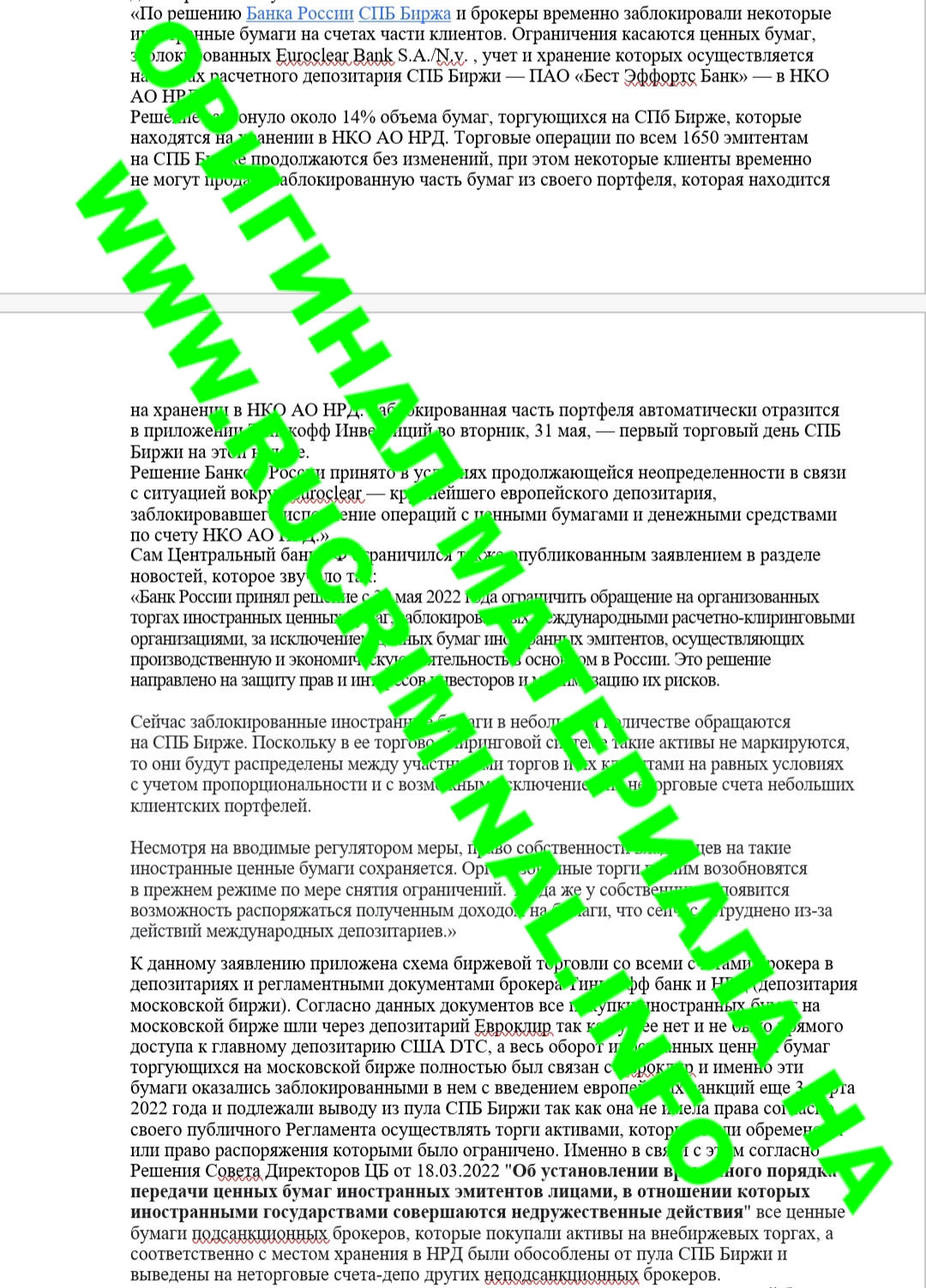

Despite the fact that not a single financial institution in the Russian Federation had direct access to DTC (the US central depository), and was forced to use the services of several intermediaries, entering the NYSE was actually a breakthrough in terms of access to a huge list of securities and low commissions. The only problem is that the rather low financial literacy of private investors, who were driven to the stock exchange in droves by the above-mentioned influencers, did not allow millions of people to assess the risks. Even if we ignore the risk, which turned out to be the most important and least expected, which will be discussed below, there was not enough literacy even to get enough information about BONY itself, which was associated with many scandals that gave rise to the status of a huge gray bank, and about the St. Petersburg Stock Exchange, not a single annual report of which was audited by the audit company of the Big 4 group. Therefore, this whole deal initially smelled good only for those who made millions on advertising stock markets in the Russian Federation. Nevertheless, 2021 brought huge profits to all securities traders due to the post-pandemic growth of the main US stock indices. Trouble awaited the investor in February 2022 with the start of the so-called special military operation of Russian President Putin. As early as 24.02.2022, full blocking sanctions were imposed on major Russian banks, including VTB Bank, Promsvyazbank and VEB RF. But further we will talk about VTB and Tinkoff banks, since it was their clients who were either completely deprived of access to their assets or were the most numerous victims. As can be seen from the text of the statements of claim in lawsuits with VTB Bank (PJSC), after the introduction of sanctions, VTB Bank (PJSC) had 30 days (from 24.02.2022 to 26.03.2022) to complete all financial transactions, including granting investors the right to sell their foreign securities. However, VTB Bank forcibly closed the opportunity to sell for its clients, citing technical problems from March 1, 2022. Later, VTB Bank sent an information message entitled "Movement of securities for the period from 24.02.2022 to 25.03.2022", which stated that the securities were transferred to the following Counterparty Banks: Alfa Bank JSC and Rosselkhozbank JSC. Brokerage service agreements were automatically concluded with Alfa Bank JSC and Rosselkhozbank JSC without the consent of VTB clients, and the securities owned by right were placed on an over-the-counter ("non-trading") account (section) of third-party banks. (In violation of clause 4.8.4. of the Terms of Depository Activities of VTB Bank PJSC.) It is worth highlighting that we are talking about shares of American companies listed on the NYSE and purchased through the St. Petersburg Exchange, against which no sanctions were imposed until November 2023. These actions to transfer the assets of VTB PJSC were carried out in accordance with the Decision of the Board of Directors of the Central Bank of the Russian Federation dated March 18, 2022, which was motivated by the blocking of assets of sanctioned brokers in Euroclear (the date miraculously coincides with the anniversary of the annexation of Crimea to the Russian Federation, and if we follow the symbolism, then, apparently, the Russian government hinted at the need to pay for the banquet at the expense of the personal funds of the middle class of the Russian Federation)

And then began three long years of endless lies from the head and employees of the Central Bank of the Russian Federation.

We should start with how the Russian stock exchange is structured. There is the Moscow Exchange, where Russian securities are traded, derivatives and debt obligations in euros were traded, as well as foreign securities in ruble valuation. Its activities are supported by the clearing center of the JSCB NCC and its central depository NCO JSC NSD. There is also PAO SPB Exchange, which traded foreign securities in US dollars through direct access to the NYSE. PAO SPB Exchange had a clearing center, OJSC "CC MFB", renamed in June 2022 to NCO CK "SPB Clearing" and a depository, PAO "Best Efforts Bank", renamed in June 2022 to PAO SPB Bank. The sanctions imposed on a broker, for example, VTB, should not have had immediate consequences for its clients, since VTB itself did not have direct contractual relations with European depositories. Contractual relations with the depositories Euroclear and Clearstream were held by the structures of the Moscow Exchange, that is, a depository of a higher order than the VTB depository, namely NSD. This is evident, among other things, from the court cases of Russian banks against Euroclear, for example, the court case of Bank Saint Petersburg, where both NSD and Euroclear were defendants, simply because the Eurobonds that were the subject of the claim were stored in Euroclear through NSD depository accounts. And until the EU Ministry of Finance imposed sanctions on NCO JSC NSD, which happened only on June 3, 2022, nothing prevented VTB Bank from closing its positions on the Moscow and Saint Petersburg Exchanges. It is also worth noting the fact that not a single court case of Russian banks against Euroclear, either in the Russian Federation or in the EU jurisdiction, which can also be found in the registers of court cases of the Russian Federation against Euroclear, concerned any shares, especially those trading on the NYSE. Each such claim dealt exclusively with Eurobonds blocked in EU structures, which indirectly confirms the general falsity of the statements of both brokers and the head of the Central Bank that the American shares of VTB clients blocked in the structures of the St. Petersburg Exchange were blocked in the Euroclear circuit, which they have repeatedly voiced. The exchange itself, obeying the sanctioning authorities, had to withdraw the assets of sanctioned banks from the pool and not have relations with them, so as not to fall under secondary sanctions. And in this case, VTB actually had to either allow clients to sell their shares and forcibly close margin positions (customers' purchase of securities using a broker's loan), or transfer the assets of clients to another unsanctioned broker. The first option is better because it excludes contractual relations between a sanctioned broker and a non-sanctioned one. Clients sold - clients are not under sanctions, no one violated anything. Therefore, Sovcombank acted exactly this way, setting deadlines for its clients for the mandatory sale of all assets.

When transferring, the new broker had to replenish the special account of the Clearing Company of the Joint Venture Exchange with the amount of funds/shares received from VTB and place securities of new clients in its depositories for depository accounting (trading and depository accounts), having checked the absence of sanctions for such new clients, the so-called compliance. But judging by the fact that the new broker placed VTB assets on off-balance sheet non-trading accounts, on which the share valuation is approximately $ 0.01, he did not receive any financial security/liquidity from VTB. This was a transfer of the register of digital rights of clients who no longer had material value from the off-balance sheet account of VTB to the off-balance sheet account of the new broker. The assets of VTB clients were simply zeroed out. It is no coincidence that the attached agreement on the transfer of assets between VTB and Alfa-Bank does not include any figures, as well as the amounts of remuneration for the transaction. Of course, there are additional agreements to them, which neither Kostin nor Fridman will ever show to anyone, even in court!

These dubious operations began to be accompanied by information noise with the emergence of a kind of financial newspeak, which did not appear in any regulatory act of the Russian Federation. Namely, "internal pool", "untagged assets", "seamless transfer", "non-trading accounts". That is, too much vocabulary appeared in the everyday life of the financial regulator, which is not provided for by any legislative act of the Russian Federation in this area. The factor of constraint and the boundaries of what is permissible disappeared in an instant, like a mask falls from a face.

The decision of the Board of Directors of the Central Bank of the Russian Federation dated 18.03.22 on the careful transfer of financial assets of citizens of the Russian Federation from an unknown place to an unknown place was naturally not the last, but only the first of three.

Tatyana Skorikova

To be continued

Source: www.rucriminal.info